With COP30 fast approaching in Brazil, I’ve been thinking about what it will take to scale renewable energy investment across Latin America. One such way is through facilitating Power Purchase Agreements (PPAs), a crucial tool for de-risking and financing renewable energy projects.

Latin America has so far, however, failed to see substantial traction in PPAs relative to European markets or the US, despite the region’s abundant energy resources and the clear financial benefits these contracts can offer.

In this piece, I’ll explore how the PPA landscape in Latin America is evolving and highlight key reasons to be optimistic about future growth. While global trends like falling technology costs and greater grid investment will help boost PPA activity everywhere, there are also region-specific drivers uniquely shaping the market in Latin America.

Market liberalisation is facilitating dealmaking across the region

The continued liberalisation of regional power markets is a key driver of accelerating PPA activity in Latin America, though activity levels and the pace of reforms vary significantly between countries.

Brazil in particular has benefitted from a favourable policy environment, making it the largest PPA market in the region. Demand is expected to grow further in the coming years after the ACL, the free market that allows offtakers to negotiate PPAs directly with generators, will allow the participation for additional industrial consumers by 2026, and eventually all consumers by 2027.

Chile has also seen substantial activity in recent years, becoming the second largest PPA market in the region. The country’s accelerating renewable energy penetration rates and new BESS reforms are now particularly leading to an interest in more sophisticated PPA deals; Grenergy signed a 24/7 solar + BESS arrangement earlier this year to supply 500 GWh annually to supply Coldeco’s copper mining operations in Chile.

Favourable market reform has not, however, been uniform across Latin America. Mexico stands out as a clear outlier, having implemented a series of reforms this year that largely rolled back the liberalisation measures introduced in 2014. This includes prioritising the dispatch of government-run, less efficient thermal plants ahead of privately owned, lower-cost renewable energy facilities. Despite this setback, the broader trend across the region continues to favour market liberalisation.

Growing volatility in hydropower generation

Latin America holds significant hydropower capacity, accounting for around 45% of total regional electricity supply. Elevated volatility in hydropower generation due to climate change has, however, increased the frequency of price spikes and power shortages. Irregular La Niña and El Niño events have further compounded the impacts on hydropower output.

Due to climate impacts, the IEA now forecasts a decline in hydropower output over the coming decades, with the regional average capacity factor over the period from 2020 to 2059 likely to decrease by around 8% on average compared to the baseline level from 1970 to 2000.

As a result of increasing hydropower variability, regional governments have increasingly turned to wind and solar PPAs to help smooth seasonal and interannual power fluctuations in hydro-dominated systems. Solar PPAs in particular serve as an effective hedge, as solar generation tends to be highest during the dry season, precisely when hydropower output is at its lowest.

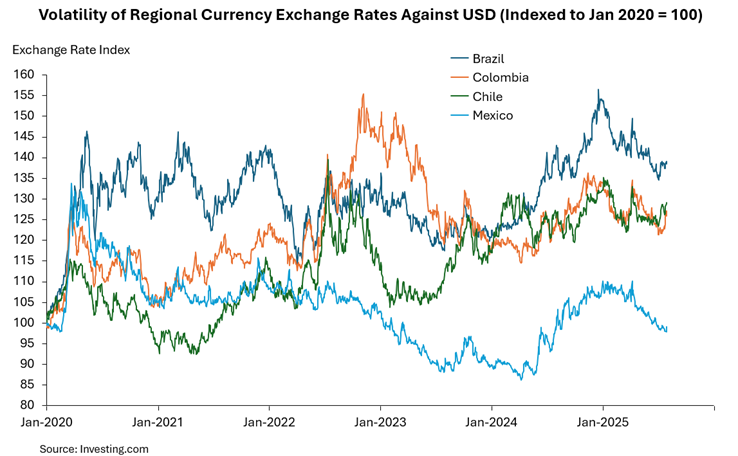

Currency de-risking is enabling PPA transactions

Currency risk has traditionally been another factor keeping PPA activity muted in Latin America. International financiers and developers are often unwilling to back projects if electricity payments are not settled in hard currency, particularly when equipment purchases are denominated in dollars or euros. A severe devaluation of the local currency can otherwise wipe out a project’s IRR, irrespective of operational performance.

PPA deals are now likely to pick up, however, as it has become increasingly common to see cash flows indexed to the euro or dollar, or even settled entirely in these hard currencies. This has been particularly true in Brazil, where activity picked up following a regulatory change at the end of 2021 that allowed PPAs to be settled in foreign currencies. Shortly after, Atlas Renewable Energy signed a 21-year USD-denominated PPA for Albras, one of the longest corporate deals signed so far in Latin America. Similar deals are likely to emerge, as these PPAs also serve as a natural hedge for export-oriented offtakers whose goods are sold in dollars.

An increasing use of derivative products, such as currency swaps or options, will also lead to growing PPA interest. While these instruments are often expensive and can reportedly amount up to 15% of total capital costs for local developers, development banks and financing institutions are increasingly lending support. Indeed, the Inter-America Development Bank reported last year it will provide $3.4 billion to support exchange rate instruments in Brazil by leveraging its investment credit rating.

Unlocking PPA growth

Latin America is poised for a surge in PPA activity. Ongoing market liberalisation, rising hydropower volatility, and the growing use of currency hedging and indexation mechanisms are all helping to unlock more transactions. With these tailwinds in place, expect PPA volumes to grow significantly in the years ahead.